I studied economics a long time ago and it continues to influence my view of the world. It partly explains my enduring frustration that economists don’t get the attention and consideration they should. So, this blog makes an appeal for more active interest in their perspective and findings.

My angst was reawakened recently when I read Oxford Economics’ analysis of the Strait of Hormuz, which warned that even a short, extreme disruption could push oil to around $140/bbl and spark wider market turmoil. It’s naive to think this assessment would have influenced decisions– but the risk and transmission channels were laid out clearly—before escalation raised the odds.

To be clear, economists covers a diverse community who’s specific forecasts are usually wrong—complex systems, changing behaviour, and external shocks ensure this. One recent study of expert forecasters found their macroeconomic calls were correct only 23% of the time. So, in advocating more listening I suggest curiosity and caution with specifics must also be applied.

It is also true the profession missed the 2008 financial crash. Economic models relied on assumptions that banks were stable and markets were self-correcting. A small minority of expert voices, however, did warn against complacency. Raghuram Rajan’s 2005 paper flagged a “small but real” risk of catastrophic meltdown; Nouriel Roubini warned at the IMF in 2006 of a housing bust and systemic crisis; and Ann Pettifor in the same year anticipated a debt‑deflationary storm in advanced economies. Outlier views at the time perhaps could have supported scenario‑thinking and risk planning.

Accepting big mistakes and the limitations of specific forecasts the economist perspective still matters a lot –and I argue warrants more attention than ever. In constructing models they reveal how systems are connected and how shocks could spread. They will recognise modern supply chains as efficient and fragile. They will value open trade (with countries specialising based on comparative advantage) as a means to improve overall prosperity. Economists offer scenarios for consideration, transmission analysis, and action trade‑offs for decision-making that can shape our collective prosperity. Above all, the analysis of economic consequences and pursuit of predicative models improve our understanding.

There were different reasons for voting Brexit, but greater UK prosperity was in all likelihood was not one. Misleading financial claims got more attention than economic analysis that was dismissed as pessimistic.

Not engaging with their findings can be expensive. UK’s Brexit provides a case-study where mainstream economics presented clear warnings. An Ipsos survey conducted in early 2016 indicated that 90% of surveyed economists expected Brexit to damage the UK economy. Before the 2016 vote, most analyses (HM Treasury, IMF, and academic work) warned that trade frictions with the UK’s largest partner would lower long‑run GDP via reduced trade, investment and productivity. Predictions differed, but a long‑run loss was commonly put in the 4–10% range depending on assumptions. A decade on, a comprehensive 2025 study (Bloom, Bunn, Mizen, Smietanka, Thwaites) estimated the UK economy is 6–8% smaller than it would otherwise have been.

More populist claims / policies necessitates more economic scrutiny

With politicians increasingly competing with populist choices and “us versus them” justifications the exploring of economic assumptions and potential outcomes is both more difficult and more important. Consider Trump’s (Supreme Court blocked) “beautiful” tariffs.

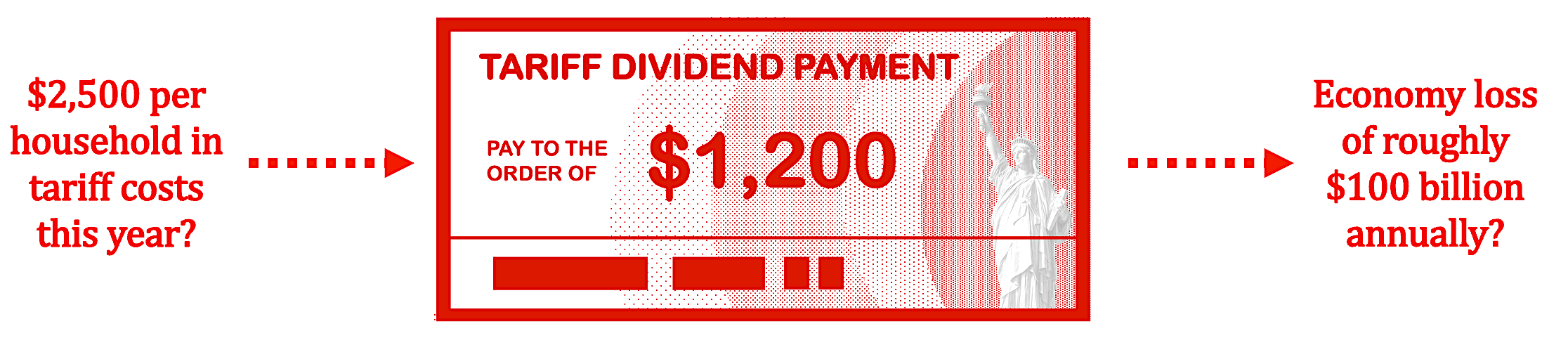

Trump had promised tariff refund “dividends” for working families (a potential payment of $1,200 or more) funded by new tariff receipts. Analysis, however, reveals (as economists expected) that U.S. firms and consumers bore c90% of the economic cost of tariffs imposed in 2025. Furthermore many forecast models (e.g. Yale Budget Lab or Penn Wharton Budget Model) project reduced GDP growth as a consequence of their introduction. Issuing a politically attention-grabbing gift of a “dividend” to voters would have therefore followed ‘invisible’ taxation and is likely to reduce America’s future prosperity.

Forecasts of US household costs and US GDP impact of course vary but the idea of families receiving a dividend is deceptive to say the least. The $2,500 is a Democrat Joint economic committee estimate and Yale estimated the $100 billion as a long run annual impact. Economic impacts of course are not limited to US.

Policymakers need economists more than ever

Some of the most challenging questions facing policymakers—such as the economic consequences of climate change or shifts in migration—are stretching what economists can model. These issues involve deeply interconnected systems where behaviours adapt and where entirely unforeseen shocks can occur. No econometric model can hope to deliver a complete answer. Each will be like a single piece of a large jigsaw picture. Despite this, they remain our best means of better understanding transmission mechanisms, magnitudes of change, which levers matter most, and what the cost of inaction might be.

Climate change is a prime example. Economists widely view it as one of the largest market failures in history: the price of fossil fuels does not reflect their true social cost, and therefore market outcomes systematically under‑price long‑term environmental damage. Proposed solutions—whether carbon pricing, regulation, or investment in alternative technologies—are often politically contentious, but the economic logic behind them is clear. By examining how markets function and where they break down, economists reveal the structural reasons climate risks accumulate.

| Negative externalities | Emitters do not bear the full social cost of their pollution, so emissions are higher than the socially efficient level. |

| Atmosphere as a public good (non‑rival, non‑excludable) | Because no one can be excluded from a stable climate and everyone can use it without reducing others’ use, markets provide no incentive for firms or countries to protect it. This leads to under‑provision of mitigation. |

| Tragedy of the commons | Everyone benefits from using fossil fuels, but the costs are shared globally, causing overuse of the atmospheric “sink.” |

| Information failures | People and firms often lack clear information about their emissions or climate impacts, leading to poor decisions. |

| Short-term incentives | Markets and governments focus on short-term gains, while climate costs are long-term, causing underinvestment in mitigation technologies. |

| Free riding | Countries benefit from others’ emission reductions, creating weak incentives to act individually and leading to global under‑provision of climate action |

Increasingly sophisticated econometric studies are improving our understanding of climate-led economic and financial risks. For example, the understanding of climate damage has developed significantly to take account of within region changes and factor in costs from extreme weather events. As the Centre for Economic Policy Research suggests recent studies are indicating that the impact on economic output might have been previously underestimated. Analysis of China’s commitment to clean energy is worthy of careful consideration too. China’s clean energy industries drove more than 90% of the country’s investment growth in 2025 and contributed to more than a third of GDP growth. The future cost of insufficient action on climate change appears to be bigger for then US and Europe when we connect wider weather impacts to clean energy capability disadvantages.

Across much of Europe, public support for reducing immigration remains high. The UK stands out as the country most likely to cite immigration as its top national concern. This anxiety is fuelled in part by a persistent overestimation of illegal immigration levels. What is often missing in public debate is a deeper understanding of the composition and economic contribution of migrants. Much analysis shows that immigration supports labour‑force growth, strengthens public finances, and boosts long‑term productivity. For example, Florence Jaumotte and IMF colleagues estimate that increasing the migrant share of the adult population by one percentage point can raise GDP per person by up to 2% in the long run. The UK’s Office for Budget Responsibility similarly finds that reduced immigration would weaken the public finances over time.

However, the economic effects of migration depend on many variables. Outcomes vary with demographics, time horizons, and the characteristics of migrants themselves—age, skills, earnings profiles, and family structures all matter. While the overall economic contribution tends to be positive, benefits can be unevenly distributed. Local pressures may emerge, such as greater competition for some low‑paid jobs or upward pressure on housing demand. This is why nuanced assessment is essential. Again, no single study provides a definitive answer: immigration’s contribution is complex, cumulative, and context‑dependent.

Despite these complexities, one conclusion is clear. Policies aimed at achieving very low or zero net migration carry economic risks, regardless of their political appeal. Skilled migrants are especially important. In the United States, for example, highly skilled migrants make up around 5% of the workforce yet account for roughly 10% of total labour income. They are also disproportionately responsible for innovation: around 23% of all US patents over the study period were produced by immigrants—about 43% above their share of STEM roles. Understanding these contributions allows policymakers to shift the conversation from net migration numbers toward net economic benefit.

I return to my appeal. Please give the findings of economists some extra attention and consideration. It might just help us avoid a further big financial mistake.

Some key sources for this article are captured below. Of course reading The Economist pointed me to some of these…

Berkeley Haas (Moore, D. & Campbell, S.)

(2024) Why economic forecasts are so often wrong. UC Berkeley Haas.

Available at: https://newsroom.haas.berkeley.edu/why-forecasts-by-elite-economists-are-usually-wrong/ [newsroom.h…rkeley.edu]

Bloom, N., Bunn, P., Mizen, P., Smietanka, P. & Thwaites, G.

(2025) The Economic Impact of Brexit. NBER Working Paper No. 34459.

Available at: https://www.nber.org/papers/w34459 [nber.org]

CEPR (Bloom, N. et al.)

(2025) Brexit’s slow‑burn hit to the UK economy. VoxEU.

Available at: https://cepr.org/voxeu/columns/brexits-slow-burn-hit-uk-economy [cepr.org]

CNBC (Iacurci, G.)

(2026) Household tariff costs: Why some families will pay more than others.

Available at: https://www.cnbc.com/2026/03/23/household-tariff-costs.html [cnbc.com]

Economonitor (Roubini, N.)

(2008) 2006 and 2007 IMF Speeches by Roubini Predicting the Recession and the Financial Crisis.

Available at: https://www.economonitor.com/nouriel/2008/08/28/2006-and-2007-imf-speeches-by-roubini-predicting-the-recession-and-the-financial-crisisand-the-five-stages-of-grief/ [economonitor.com]

IMF (Jaumotte, F., Koloskova, K. & Saxena, S.)

(2016) Migrants Bring Economic Benefits for Advanced Economies. IMF Blog.

Available at: https://www.imf.org/en/blogs/articles/2016/10/24/migrants-bring-economic-benefits-for-advanced-economies [imf.org]

National Bureau of Economic Research (Rajan, R.)

(2005) Has Financial Development Made the World Riskier? NBER Working Paper No. 11728.

Available at: https://www.nber.org/papers/w11728 [nber.org]

Oxford Economics

(2026) Iran war scenarios: The oil price that breaks parts of the economy.

Available at: https://www.oxfordeconomics.com/resource/iran-war-scenarios-the-oil-price-that-breaks-parts-of-the-economy/ [oxfordeconomics.com]

UC Press / Collabra Psychology (Campbell, S. & Moore, D.)

(2024) Overprecision in the Survey of Professional Forecasters.

Available at: https://online.ucpress.edu/collabra/article/10/1/92953/200113/Overprecision-in-the-Survey-of-Professional [online.ucpress.edu]

Yale Budget Lab

(2026) Tracking the Economic Effects of Tariffs.

Available at: https://budgetlab.yale.edu/research/tracking-economic-effects-tariffs [budgetlab.yale.edu]

Carbon Brief (Evans, S.)

(2026) Analysis: Clean energy drove more than a third of China’s GDP growth in 2025.

Available at: https://www.carbonbrief.org/analysis-clean-energy-drove-more-than-a-third-of-chinas-gdp-growth-in-2025/

Joint Economic Committee (U.S. Congress)

(2026) Fact Sheet: The Cost of Tariffs for Families in 2026.

Available at: https://www.jec.senate.gov/public/_cache/files/4836e257-91a5-426b-95bb-3e575a855f5b/jec-fact-sheet-on-cost-of-tariffs-for-families-2026.pdf

Pettifor, A.

(2006) The Coming First World Debt Crisis. Palgrave Macmillan.

DOI: https://doi.org/10.1057/9780230236752

Bernstein, S., Diamond, R., Jiranaphawiboon, A., McQuade, T. & Pousada, B.

(2025) The Contribution of High-Skilled Immigrants to Innovation in the United States. Working paper, 16 December 2025.

Neal, T., Newell, B. & Pitman, A.

(2025) Reconsidering the macroeconomic damage of severe warming. Research paper.

Institute for Fiscal Studies (Johnson, P.)

(2016) Leavers may not like economists but we are right about Brexit. Institute for Fiscal Studies.

Available at: https://ifs.org.uk/articles/paul-johnson-leavers-may-not-economists-we-are-right-about-brexit